Money has a way of disappearing fast when there is no clear plan for it. One day you get paid, and a few days later it feels like half of it is already gone. Bills, groceries, small treats, transport, subscriptions, and random little expenses all start piling up. That is why learning how to budget money can make such a huge difference in your life. A budget gives your money a job before you spend it, so you feel more in control and less stressed.

A lot of people think budgeting means cutting out everything fun and living under strict rules. That is not true. A good budget is not punishment. It is a tool that helps you manage your income, cover your needs, enjoy some wants, and work toward your goals. Once you understand the basics, budgeting money becomes much less scary and much more useful.

What Does It Mean to Budget Money?

To budget money means to create a simple plan for how you will use your income. It helps you decide how much will go toward bills, food, savings, debt, transport, and personal spending. Instead of wondering where your money went at the end of the month, you already know where it was supposed to go from the start.

A budget does not need to be fancy. It can be written in a notebook, made in a spreadsheet, or tracked in an app. The format matters less than the habit itself. What really matters is that you can clearly see your income, your expenses, and your priorities.

Budgeting also works no matter how much money you earn. Some people think budgets are only for people who are struggling. In reality, everyone can benefit from one. If your income is high, a budget helps you grow savings and avoid waste. If your income is tight, a budget helps you survive smarter and reduce financial pressure.

Why Budgeting Money Is Important

Budgeting is important because it gives you clarity. Without a budget, money often gets spent in small pieces that feel harmless in the moment. A coffee here, a food delivery there, a random online order, and suddenly your account balance looks much smaller than expected. A budget helps you notice these patterns before they become a real problem.

It also helps you prepare for regular bills and future goals. When you budget, rent or groceries stop feeling like surprise expenses because you already planned for them. On top of that, you make room for savings, emergency funds, debt payments, and future purchases. Budgeting creates a sense of direction.

Another big reason budgeting matters is the peace of mind it brings. Financial stress affects your mood, sleep, relationships, and daily decisions. When you know your numbers and have a plan, even a simple one, you feel calmer. You may not fix everything overnight, but you stop feeling like your money is always controlling you.

Signs You Need a Budget

Many people need a budget long before they realize it. One common sign is not knowing where your money goes each month. If you earn money regularly but still feel confused about why there is never enough left, that is a strong clue. It usually means your spending is happening without enough attention.

Another sign is running short before the month ends. If you often feel broke in the last week before payday, your money may not be spread out in a realistic way. The same goes for relying too much on credit cards, borrowing from friends, or dipping into savings just to cover normal expenses.

You may also need a budget if you want to save but never seem to start. Many people think saving will happen naturally once there is extra money left over. In real life, that extra money often disappears unless you plan for it. A budget helps you make saving intentional instead of accidental.

Step-by-Step Guide on How to Budget Money

1. Calculate Your Total Monthly Income

The first step in budget planning is knowing exactly how much money comes in each month. This includes your salary, freelance income, side hustles, regular support, or any other steady money you receive. Use the amount you actually take home after tax, not the bigger number you see before deductions.

This step sounds simple, but it matters a lot. If you base your budget on income that is not consistent or not yet in your account, you may build a plan that falls apart quickly. Be honest and use the most realistic number possible.

If your income changes from month to month, you can use your average income from the last few months or start with your lowest usual month. That gives you a safer number to work with and helps prevent overspending.

2. Track Your Monthly Expenses

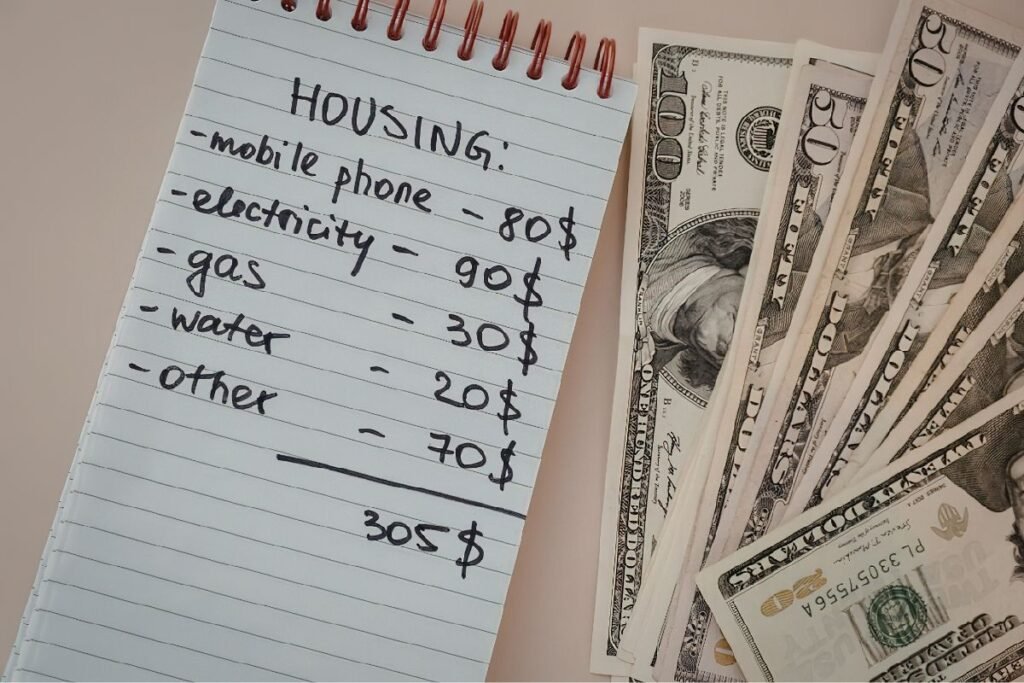

Once you know your income, the next step is to see where your money is going. Start by listing all your regular expenses. These may include rent, electricity, internet, transportation, groceries, loan payments, school fees, insurance, subscriptions, childcare, and mobile bills.

Then look at your variable expenses. These are the ones that change more often, such as eating out, shopping, gifts, entertainment, personal care, and small daily purchases. Many people underestimate this category because the spending feels minor in the moment.

Tracking your expenses shows the truth. Sometimes that truth is uncomfortable, but it is also helpful. You cannot improve what you do not see. Once your spending is visible, you can start making better choices without guessing.

3. Separate Needs From Wants

This is one of the most important steps in learning how to make a budget. Needs are the expenses you must pay to live and function, such as housing, food, transport, healthcare, and utilities. Wants are the extras that make life enjoyable but are not essential for survival.

The tricky part is that some expenses can feel like needs when they are really wants. For example, basic groceries are a need, but frequent food delivery may be a want. A phone bill may be a need, but paying extra for a more expensive plan than necessary might be a want.

This step is not about removing all joy from your life. It is about understanding the difference between essential spending and optional spending. Once you know that, you can adjust your money with more confidence and less guilt.

4. Set Clear Financial Goals

Budgeting becomes much easier when you have a reason behind it. That is where goals come in. A short-term goal could be saving for school supplies, paying an upcoming bill, or building a small emergency fund. A long-term goal could be paying off debt, buying a car, moving out, or saving for retirement.

Goals help your budget feel purposeful. Without goals, budgeting can feel like a boring list of limits. With goals, it becomes a plan that supports something meaningful. That shift changes everything.

Try to make your goals specific and realistic. “Save more money” is too vague. “Save $300 in three months” is clearer and easier to work with. A simple target gives you something to aim at each month.

5. Choose a Budgeting Method

There is no one perfect budgeting method for everyone. The best method is the one you can actually stick with. Some people like structure and detailed tracking. Others want something simple and flexible.

You can try the 50/30/20 rule, zero-based budgeting, envelope budgeting, or a pay-yourself-first approach. Each method works differently, but they all aim to help you manage your money with more intention.

Do not worry about finding the perfect system right away. It is better to choose a simple method and start than to keep waiting for a perfect plan you never use.

6. Create Spending Categories

Now it is time to divide your money into categories. Common budget categories include housing, food, transportation, debt payments, savings, healthcare, personal spending, entertainment, and emergency funds.

These categories help you organize your money in a way that makes sense. Instead of seeing one big number, you break it into smaller parts. That makes your budget easier to understand and easier to follow.

Your categories do not need to look exactly like someone else’s. A student, a parent, and a freelancer may all need different budget categories. The important thing is to create categories that fit your real life.

7. Set Limits for Each Category

Once you have categories, assign a realistic amount to each one. This is where your budget becomes more practical. Based on your income and past spending, decide how much you can spend in each area.

Try not to make your limits too strict in the beginning. A budget that looks perfect on paper can still fail if it feels impossible in real life. If you usually spend a certain amount on groceries or transport, do not slash it unrealistically unless you have a clear plan for how to adjust.

A budget should guide you, not trap you. It is okay to fine-tune your numbers over time. Realistic limits make it easier to keep going.

8. Review and Adjust Weekly

A budget is not something you make once and forget. It works best when you check in on it regularly. A short weekly review can help you see what you have spent, what is left, and where you may need to slow down.

These check-ins prevent end-of-month panic. They help you notice problems early, such as overspending in one category or forgetting a coming bill. That gives you time to adjust before things get messy.

Weekly reviews also help you stay emotionally connected to your goals. It is easier to make smart choices when your plan is fresh in your mind instead of buried somewhere you never look at.

9. Build Saving Into Your Budget

Saving should not be treated like an afterthought. If you wait to save whatever is left at the end of the month, there is often nothing left. That is why it helps to treat savings like a bill that must be paid.

Even a small amount matters. You do not need to save huge amounts to start building better habits. A little saved consistently can do more than a big amount saved once and then forgotten.

Automatic transfers can make this easier. When money moves into savings without you having to think about it, you are less likely to spend it. This is one of the simplest money budgeting tips that actually works.

10. Prepare for Unexpected Expenses

Life rarely follows a perfect plan. A budget works better when it includes space for surprises. This may be a medical cost, a repair, a gift, an urgent trip, or a school-related expense you forgot was coming.

That is why adding a small buffer to your budget is smart. It gives you breathing room. Over time, building an emergency fund can protect you from bigger setbacks too.

Unexpected expenses are not always truly unexpected. Many of them happen every year in some form. A better budget does not pretend life will be smooth all the time. It prepares for bumps in the road.

Popular Budgeting Methods

The 50/30/20 Budget Rule

This method divides your income into three parts. About 50 percent goes to needs, 30 percent goes to wants, and 20 percent goes to savings or debt payments. It is popular because it is simple and easy to remember.

This method works well for people who want a flexible structure without tracking every tiny detail. It gives a broad guideline while still leaving room for personal choices. The percentages do not need to be perfect, but they give a useful starting point.

Zero-Based Budgeting

In zero-based budgeting, every dollar has a job. You assign all your income to a category until there is nothing left unplanned. That does not mean spending everything. It means some of your money may be assigned to savings, debt, or future goals.

This method works well for people who want close control over their money. It takes more attention, but it can be very effective if you tend to lose track of where your money goes.

Envelope Budgeting

This method uses separate envelopes for spending categories like groceries, transport, or entertainment. You place cash in each envelope and stop spending once it is empty.

This can be very useful for people who overspend easily with cards or apps. Physically seeing the money run out can change behavior faster than looking at numbers on a screen.

Pay Yourself First

This method focuses on saving first before spending on other things. As soon as your income arrives, you move part of it to savings. Then you manage the rest.

It is a strong method for people who struggle to save consistently. It helps make saving a priority instead of a leftover idea.

How to Budget Money on a Low Income

Budgeting on a low income can feel especially hard because there is less room for error. When most of your income already goes toward basics, even small unexpected expenses can hit hard. That is why your budget needs to be very clear and very honest.

Start with essentials first. Housing, food, transport, utilities, and healthcare come before everything else. Then look carefully at small spending leaks. These might be minor on their own, but together they can take a surprising amount from your budget.

It is also important to be kind to yourself. Budgeting on a low income is not about magically fixing everything. It is about helping your money stretch further, avoiding waste, and creating a little more control. Even saving a tiny amount matters. Progress counts, even when it feels slow.

Best Budgeting Tools and Apps

You do not need a fancy app to make a budget work. A notebook can work. A basic spreadsheet can work. Even a simple note on your phone can work if you use it consistently.

That said, some people find tools helpful because they make tracking easier. Budgeting apps can categorize spending automatically, remind you about bills, and show progress in a visual way. Bank apps may also include spending summaries that help you see where your money goes.

Choose a tool that feels simple enough to stick with. The best budget tool is not the most advanced one. It is the one you will actually open and use every week.

Common Budgeting Mistakes to Avoid

One common mistake is making the budget too strict from the start. When the plan feels harsh and unrealistic, people often give up quickly. A budget should challenge bad habits, but it should still fit real life.

Another mistake is forgetting irregular expenses. Things like birthdays, school fees, seasonal shopping, repairs, and health costs may not happen monthly, but they still need to be planned for. Ignoring them can throw your budget off balance.

People also make the mistake of giving up after one bad month. A budget is not ruined because you slipped up. One rough month does not mean you failed. It just means your plan needs adjustment. Budgeting works better when you treat it like a skill you are building, not a test you either pass or fail.

Budgeting Tips for Beginners

If you are just starting, keep it simple. Use rounded numbers if that helps. Focus on awareness before perfection. You do not need a complicated system to make progress.

Review your spending at the same time each week so it becomes a habit. Keep your financial goals visible somewhere you can see them. That reminder makes small daily choices easier. If you are trying to save or pay off debt, celebrate small wins instead of waiting for a huge breakthrough.

Most of all, be patient with yourself. Budgeting is not something most people learn overnight. Like cooking or driving, it gets easier with practice. The more you repeat the process, the more natural it feels.

Sample Simple Monthly Budget

A simple monthly budget helps you see exactly where your money is going. It does not need to be complicated. The goal is to give every major expense a place so you can manage your money with less stress and more confidence.

For example, if your monthly income is $2,000, your budget might look like this:

| Category | Amount |

|---|---|

| Monthly Income | $2,000 |

| Rent and Utilities | $800 |

| Groceries | $250 |

| Transportation | $150 |

| Debt Payments | $200 |

| Savings | $200 |

| Phone and Internet | $100 |

| Personal Spending | $150 |

| Entertainment | $75 |

| Emergency Buffer | $75 |

This kind of layout helps you see your money clearly. It does not need to be perfect. The point is to give every major expense an amount so your income has a plan. Your numbers may look very different, and that is fine. What matters is building a plan around your real situation.

FAQs About How to Budget Money

How do beginners start budgeting money?

Beginners can start by listing their monthly income and expenses. Then they can separate needs from wants, choose spending categories, and set simple limits for each one.

What is the easiest budgeting method?

The 50/30/20 rule is often the easiest because it is simple to understand and does not require detailed tracking of every small purchase.

How much money should I save each month?

That depends on your income and expenses. Even a small amount is worth saving. The key is consistency, not perfection.

How do I budget money on a low income?

Focus on essentials first, track every expense carefully, reduce small unnecessary spending, and save even tiny amounts when possible.

Can I budget without using an app?

Yes, absolutely. A notebook, spreadsheet, or printed planner can work just as well as an app if you use it regularly.

How often should I review my budget?

A weekly check-in works well for most people. It helps you stay aware of your spending and fix small issues before they grow.

Why do budgets fail?

Budgets often fail because they are too strict, not reviewed often, or not built around real spending habits. A better budget is realistic and flexible.

Conclusion

Learning how to budget money is one of the most useful personal finance skills you can build. It helps you understand your spending, reduce stress, save with more purpose, and make smarter decisions month after month. A budget does not need to be complicated to work. It just needs to be honest, realistic, and used consistently.

Start with your income. Track your expenses. Separate needs from wants. Set a few simple goals and build from there. Small changes add up. The sooner you begin, the sooner your money starts feeling less chaotic and more manageable.